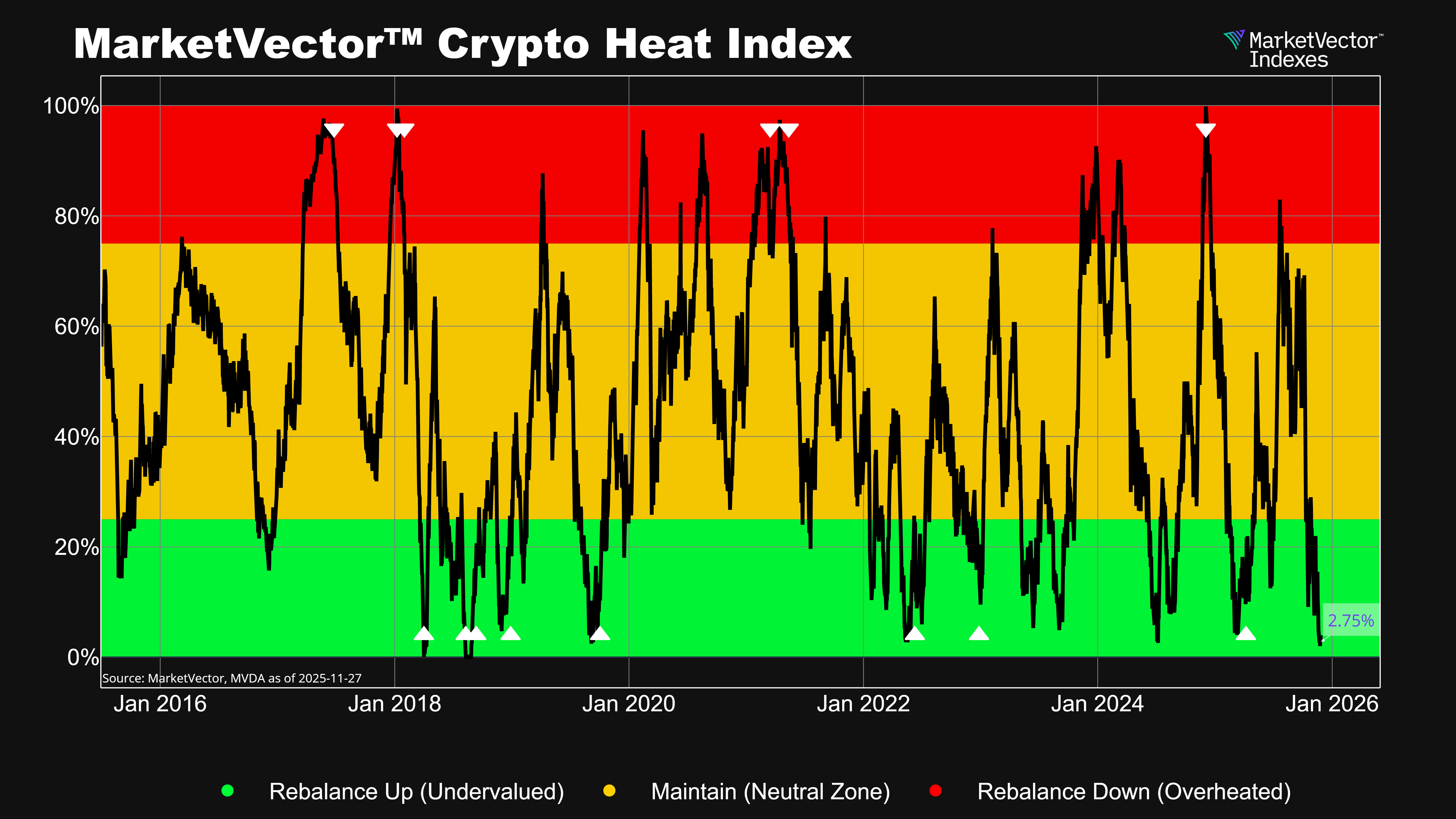

The crypto asset market has been dominated by retail investors, with specialized hedge funds and family offices also participating. This once-in-a-lifetime market has revealed that not only has the ordinary Joe or Jane failed to capitalize on buying and selling opportunities, but some of the most notable hedge funds in the field failed to implement effective risk management. The crypto market cycles, both up and down, exhibit the characteristics of financial bubbles.

Understanding how market cycle function can help you retain perspective during times of uncertainty, allowing you to concentrate on your investment strategy based on your own objectives. Using Bitcoin to Identify the Crypto Market Cycle is a good starting point.

For this analysis, the following lessons can be drawn:

- Successive cycles produce diminishing returns and last longer. Since the cryptocurrency market is expanding, bull runs are taking more time to complete. It's not out of the ordinary for the peak to be reached after more than three years.

- The current bear market is the second largest in terms of duration, hitting the 400 days mark. However, it remains only the second longest so far. Bitcoin is currently down 75%, which is slightly less than the 85% we saw in the previous two cycles. However, the severity of the last two bear markets suggests that the low was preceded by a rapid liquidation event. It's an educated guess whether we\ve seen that already.

- Time to recover can take years. In the worst-case scenario, recouping your losses may take more than three years.

- Small cap tokens as defined by our MVIS® CryptoCompare Digital Assets 100 Small-Cap Index (ticker: MVDASC) still have a larger drawdown and not necessarily a higher return than large cap token such as Bitcoin and Ethereum. It’s fair to say that the performance is more related to the life cycle and nascency; this is more related to startup risk than size risk.

MVIS® CryptoCompare Digital Assets 100 Small-Cap Index

19/12/2021-19/12/2022

Source: MarketVector IndexesTM, data as of December 19, 2022.

This topic is explored in some more detail in a whitepaper published in our MVIS Insights of “Crypto Market Cycles - What goes up must come down.pdf”.

Get the latest news & insights from MarketVector

Get the newsletterRelated: