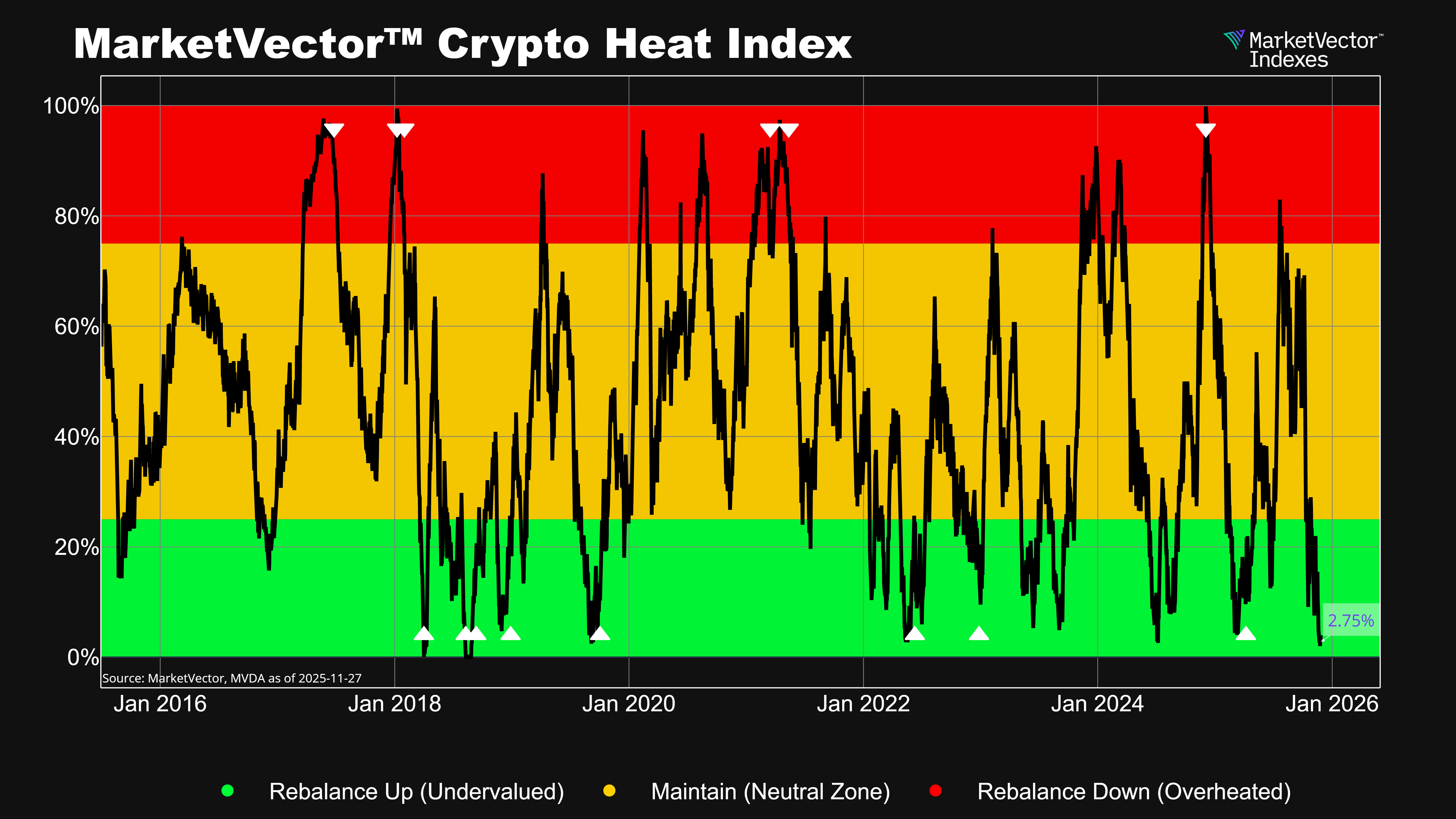

What is a reasonable investment in digital assets? Taking into account liquidity, name recognition and market capitalization, bitcoin represents the simplest solution. However, investors have an understandable desire for a minimum level of diversification. Achieving this goal without unintentionally increasing the portfolio's risk is no easy task.

The current crypto assets are early manifestations of potentially forward-looking protocols, but no one can know if and how they will hold up in an environment of constant evolution. Some tokens may catch on, but many of the future winners probably don't even exist yet. The current development phase is comparable to the early phase of the Internet in the early 1990s. Companies like Google or Amazon did not exist at that time, but they dominate today's web. By contrast, AltaVista, Lycos or Netscape didn’t survive.

It is therefore important to think in terms of probabilities rather than dogmatically. Bitcoin is the only finished product we have. Thus, it has the greatest chance to survive going forward. The uncertainty is already greater with Ethereum, simply because of the serious competition.

In crypto, the passive approach of buying an asset and holding it forever is called "hodl". This designation resulted from a misspelling in a forum post. Amidst falling prices, a frustrated investor wrote "I am hodling" on the bitcointalk.org site in December 2013. Of course, what was meant was "holding." Meanwhile, "hodl" translates to "hold on for dear life," an approach that reaps rewards in a long-term up market. An elaborate investment strategy with sound risk management looks different.

In assessing how useful a "hodl" strategy would have been in the past, it helps to look at the performance of the top 10 token over time. Apart from Bitcoin, the composition is pretty unstable. The high dispersion of the ranking is striking. Bitshares, for example, is now ranked 469th and Paycoin even dropped to 2524th place within a few years. The following table shows the top ten token of the last nine years. The ranking in March 2022 is noted in brackets.

Top 10 Token Every Year

Source: MV Index Solutions. Coinmarketcaps. Data as of March 2022.

Of the top 50 coins in 2015, 34 aren’t even in the top 500, 16 of them have become so small and insignificant that they aren’t able to be traded on any mainstream exchange today, and 11 don’t even exist. This has all taken place in just seven short years.

Thus an investor may pursue a systematic approach to capture the market performance. A market capitalization based index is a simple way to earn the market performance of the crypto assets. This weighting method is comparable to a long-term trend follower. The winners are bought and increase in weight, while the losers are reduced. This approach is not free of weaknesses either, but it is a good starting point.

“To repeat, while such an index-driven strategy may not be the best investment strategy ever devised, the number of investment strategies that are worse is infinite.”

John Bogle, The Little Book of Common Sense Investing

At MVIS, we cap the maximum weight per token in order to get a diversified index. Liquidity criteria help to construct an index, which is investable. Our MVIS CryptoCompare Digital Assets 10 Index is a modified market cap-weighted index which tracks the performance of the 10 largest and most liquid digital assets.

Get the latest news & insights from MarketVector

Get the newsletterRelated: