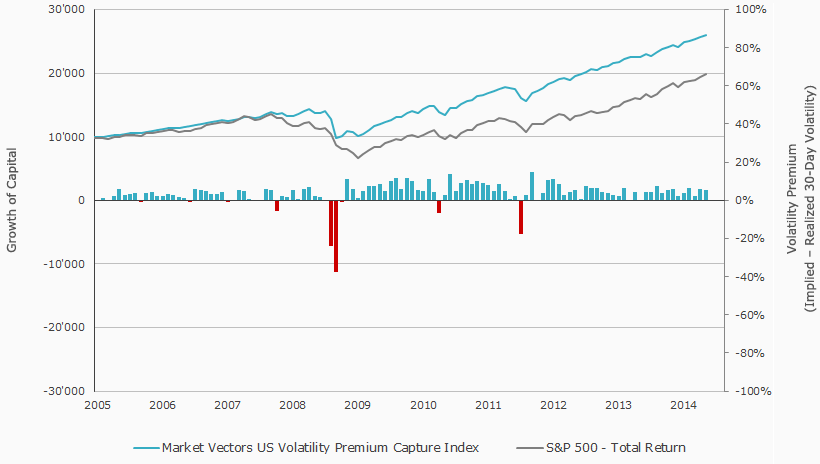

By generating consistent performance and limiting drawdowns, simple equity index put option-writing strategies have historically earned outsized risk-adjusted profits compared with buy-and-hold investments in the underlying index. Writing put contracts typically results in the receipt of a large premium to insure the downside of the index, regardless of the absolute level of volatility. However, volatility spikes often result in capital losses, due to temporarily negative premiums, until option prices re-adjust to reflect the risk. Once the risk subsides, the premiums typically remain elevated for an extended period of time and this often allows the writers of put option contracts to recover quickly from drawdowns.

Source: Bloomberg

Data as of 30 Sep 2014

- Market Vectors® US Volatility Premium Capture Index is a rules-based index that reflects out-of-the-money put-options on SPY. The index seeks to control risk by adjusting the strike prices of puts by incorporating predicted volatility, has 4 buckets selling puts expiring 1-2m out from front month, each spaced apart by one week, each bucket has same notional exposure, strike and expiry vary. Cash in 3-m T-Bills.

- S&P 500® Index is an unmanaged and market-value weighted index which includes a representative sample of 500 companies in leading industries of the U.S. economy. The diverse index comprises over 70% of the total market capitalization of all stocks traded in the U.S.

- Implied volatility is measured via the CBOE Volatility Index (VIX). The VIX index reflects a market estimate of future volatility, based on the weighted average of the implied volatilities for a wide range of strikes. 1st & 2nd month expirations are used until 8 days from expiration, then the 2nd and 3rd are used.

- Realized Volatility is calculated as the annualized 30-day standard deviation of the S&P 500 Index.

Get the latest news & insights from MarketVector

Get the newsletterRelated: