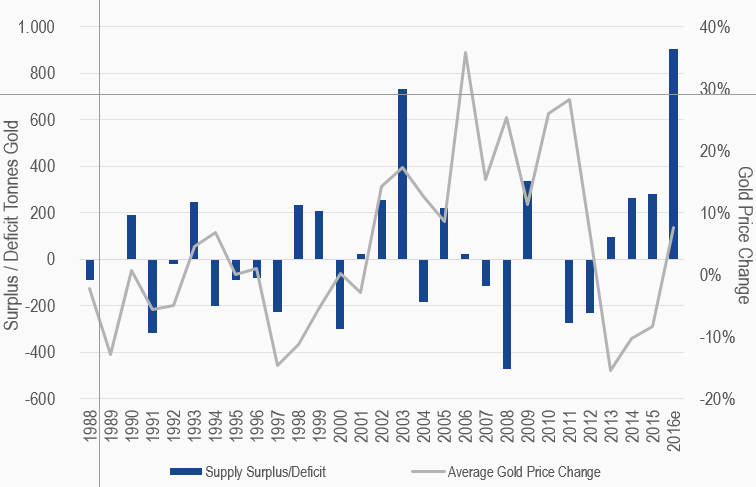

The Price of Gold is not Driven by the Same Supply/Demand Fundamentals as Many Other Commodities.

Since 1988 there are many years when the gold price rose when there was a physical surplus. Likewise, there are also years when the price fell and there was a deficit. We believe there are three possible reasons for this:

- The global physical gold market is difficult to measure accurately

- The huge above ground stores of gold

- Investment drivers in the paper gold market can overwhelm the physical market

As 88% of global trading volume occurs in New York and London, we believe the dominant driver of gold prices is Western investment demand. Western investors and others use gold to monetize their views on currencies, interest rates, geopolitical risk, systemic financial risk, central bank policies, inflation, deflation, and tail risk.

Gold Supply versus Price Change

1988-2016

Source: Thomson Reuters GFMS; Bloomberg; Vaneck. Data as of December 31,2016.

Not intended to be a forecast of future events, a guarantee of future results or investment advice.

Current market conditions may not continue.

About the Author:

Joe Foster has been Portfolio Manager for the VanEck International Investors Gold Fund since 1998 and the VanEck – Global Gold UCITS Fund since 2012. Mr. Foster, an acknowledged authority on gold, has over 10 years of dedicated experience in geology and mining including as a gold geologist in Nevada. He has appeared in The Wall Street Journal, Barron's, and on Reuters, CNBC and Bloomberg TV. Mr. Foster has also published articles in a number of mining journals, including Mining Engineering and Geological Society of Nevada.

The article above is an opinion of the author and does not necessarily reflect the opinion of MV Index Solutions or its affiliates.